| |

Accounting Period ConceptWhat is the accounting period concept?According to the Accounting Period Concept, accounting activities should be separated into smaller intervals to measure business performance. One year is the standard accounting time for reporting the performance of the business to outsiders. Most corporations must produce an annual report to their shareholders and income tax filing every year. The accounting year or fiscal year correlates to the calendar year in most enterprises. However, many organizations employ the natural business year rather than the calendar year.

A calendar year or economic year is an accounting length, a hard and fast length in which accounting sports are performed, collected, and analysed. The accounting length is vital in funding because capability shareholders compare a company`s overall performance with the use of monetary statements primarily based totally on a predetermined accounting length. The accounting period is usually three, six, or twelve months, and other corporate entities adhere to a three or six-month accounting period. For internal purposes, the accounting period is assumed to be one month or one quarter, even though externally, the accounting period is twelve months. Instead of an entire year, the International Financial Reporting Standards (IFRS) allow 52 weeks, referred to as the financial year as an accounting term. Important Accounting Points

Accounting period illustration'Ram & Sons' is in the clothing business. According to the going concern idea, the company will continue to operate indefinitely. So, according to the accounting period concept, Ram & Sons prepares their accounts once a year, with the year beginning on April 1 and ending on March 31.

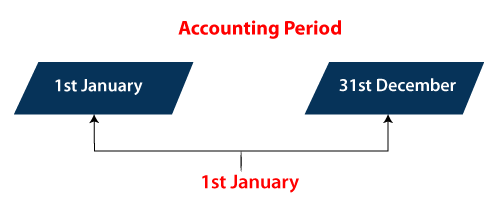

What are the different types of accounting periods?1. The Calendar Year The accounting period corresponds to the 12-month Gregorio calendar year. The calendar runs from January 1st to December 31st, and this 12-month natural progression is followed by an accounting period. 2. The Fiscal Year A fiscal year is a year that does not end on December 31st. International Financial Reporting Standards (IFRS) generally allow an accounting period of 52 weeks. Companies that adhere to the 52 or 53-week fiscal cycle benefit from financial tracking and reporting. The Internal Revenue Service (IRS) allows taxpayers to record taxes by calendar year or fiscal year. If the company wants to switch from the calendar to the fiscal year, the IRS must grant permission. 3. Calendar Year 4-4-5 It is the most typical calendar format, particularly in retail and manufacturing. A year is divided into four halves according to the 4-4-5 calendars, and each quarter consists of 13 weeks divided into a five-week months and two four-week months. This data is essential for business owners, investors, creditors, and government agencies. The period assumption provides stakeholders with reliable and relevant financial information to make timely business choices. The accounting period is determined by the business requirements and conditions, which may be too complex to warrant different accounting periods. Therefore, all companies are free to set as many deadlines as they need to comply with the law. Accounting Period Concept IssuesBusinesses are living, breathing entities. The continuous stream of trading events can be optionally divided into phases. Because business activities do not cease or drastically change when one accounting period finishes and another begins. Because of this, the challenge of calculating income for an accounting period is the most challenging in accounting. Provisional reportsManagement needs information more than once a year. As a result, management income statements are prepared more regularly. A month is the most usual period, but it can be as brief as a week or even a day. Why is an Accounting Period necessary?Accounting periods provide executives with ongoing insights into the company's profitability and help them make informed business decisions. Accountants created the periodicity idea to enable this. Using this idea, ongoing and complicated business activities are separated into short periods and reported in monthly quarterly and yearly financial statements. The company creates and publishes a financial account for each period. The period of the financial statements is stated in the heading. This data is helpful to business owners, investors, creditors, and government agencies. The period assumption provides stakeholders with reliable and relevant financial information to make timely business choices. The accounting period selected depends on the needs and circumstances of the company. It can be complicated enough to justify different accounting periods. All companies are free to define any number of periods if legal standards are met. How an accounting period functions?At any particular point in time, many accounting periods usually are active. For example, a company may close its books in June, which means the accounting period is a month (June). Still, companies may want to aggregate their accounting data quarterly (April-June), half (January-June), and calendar year. Accounting Period RequirementsConsistencyAccounting periods are defined for reporting and analysis. Theoretically, a company wants to see consistent growth across all accounting periods to show stability and a long-term earnings outlook. Accrual accounting is an accounting approach that supports this premise. Accrual accounting methods require accounting input each time an economic event occurs, regardless of when the monetary component of the event occurs. For example; in accrual accounting, fixed assets are depreciated over their useful life. In contrast to the comprehensive view of spending when an item is paid, this payment identification allows for relative comparisons over several billing periods. Matching principleMatching principles are important accounting rules related to the use of accounting periods. The matching principle mandates that expenses be recorded in the accounting period in which they were incurred, as well as any associated income received as a result of those expenses. For example; the period used to report the cost of an item sold is the same as the period used to report the revenue of the same item. According to the matching principle, the financial data recorded in a fiscal period is as complete as possible and should not be spread across multiple accounting periods. Accounting Period Concept ExamplesExample - 1 Every year, a corporation records its transactions from January 1st to December 31st and then closes its books. The billing period, in this case, is one year, from January 1st to December 31st. However, not all businesses must adhere to a single year. Example - 2 A corporation records its transactions from January 1st to June 30th of each year and then closes its books of accounts. The accounting period, in this case, is half a year, from January 1st to June 30th, and the next period is from July 1st to December 31st. AdvantagesThe following are advantages and benefits to financial statement users:

DisadvantagesHere are following disadvantages to financial statement users:

Accounting period and fiscal yearThe accounting period has no set length and might be as short as one year or as long as more than one year. It can be divided into two types: calendar year and fiscal year. Therefore, you can start on the 1st of every month. On the other hand, the fiscal year is from April 1st to March 31st. Therefore, the total length of the fiscal year is one year, and unlike the accounting period, which can be shortened or extended by one year, the start and end dates are fixed and cannot be changed. ConclusionCompanies need to choose their accounting periods intelligently and should not change them unless circumstances require such changes. All linked accounting transactions must be recorded in the same period, and mandatory accounting rules must be established to avoid violating matching principles.

Next TopicDebit Meaning in Accounting

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share