| |

Advantages and Disadvantages of Marginal CostingThe marginal cost in economics is the variation in total production costs that results from creating or producing one more unit. Subtract the change in production costs from the change in quantity to determine marginal cost. In order to maximise production and overall operations, an organisation needs to know when it can achieve economies of scale. This is the goal of marginal cost analysis. A profit could be made by the producer if the marginal cost of producing one extra unit is less than the price per unit.

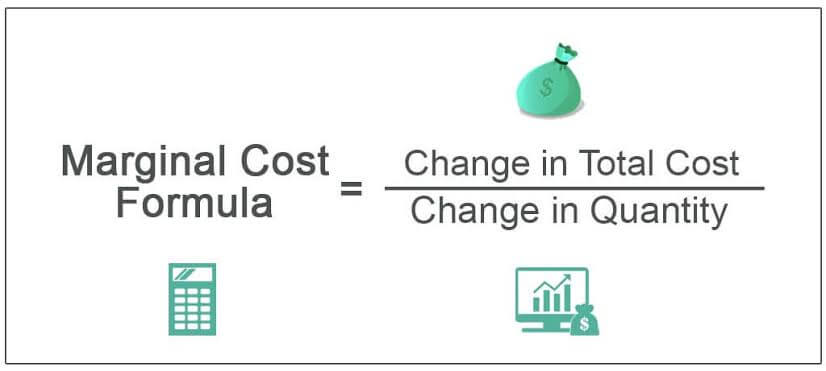

Marginal Cost Formula

Marginal cost is calculated as the total expenses required to manufacture one additional good. Therefore, it can be measured by changes to the expenses incurred for any given additional unit. Marginal Cost = Change in Total Expenses / Change in Quantity of Units Produced When producing multiple additional units, the formula above can be used. However, management must be aware that different production unit groups may have marginal costs that are materially different from one another. Manufacturers most frequently employ the economics and managerial accounting concept of marginal cost to determine the optimal production level. When planning their production schedules, manufacturers frequently calculate the cost of adding one more unit. At a certain point in production, the advantage of producing one extra unit and earning money from that product will lower the total cost of manufacturing the product line. Finding that point or level as soon as possible is essential for manufacturing cost optimization. Marginal cost includes all of the costs that vary with that level of production. For example, if a company needs to build an entirely new factory in order to produce more goods, the cost of building the factory is a marginal cost. The amount of marginal cost varies according to the volume of the good being produced. Marginal cost is an important factor in economic theory because a company that is looking to maximize its profits will produce up to the point where marginal cost (MC) equals marginal revenue (MR). Beyond that point, the cost of producing an additional unit will exceed the revenue generated. Example of Marginal CostProduction costs consist of both fixed costs and variable costs. Fixed costs do not change with an increase or decrease in production levels, so the same value can be spread out over more output units with increased production. Variable costs refer to costs that change with varying levels of output. Therefore, variable costs will increase when more units are produced. Special ConsiderationsThe relationship between marginal revenue and average cost is frequently graphically represented as the marginal cost. The marginal cost slope varies depending on the company and the product, but it frequently takes the form of a "U" curve that initially declines as efficiency is realized before possibly exponentially rising later. Advantages of Marginal Costing1. Constant in nature While variable costs occasionally change, marginal costs are stable over the long term. Regardless of the level of production, margin costs are constant. 2. Effective cost control It divides cost into fixed and variable. Fixed cost is excluded from product. As such, management can control marginal cost effectively. 3. Simplified treatment of overheads By separating fixed overheads from production costs, it lessens the degree to which overheads are over- or under-recovered. 4. Uniform and realistic valuation As the fixed overhead costs are excluded from product costs, the valuation of work-in-progress and finished goods becomes more realistic. 5. Helpful to management Management finds it helpful because it makes it possible to launch a profitable new production line. Finding out whether to buy or manufacture a product helps determine the more profitable one. Regarding pricing and tendering, management has the final say. 6. Helps in production planning It shows the amount of profit at every output level with the help of the cost-volume-profit relationship. Here the break-even chart is made use of. 7. Decision-making Marginal costing helps management with adequate information appropriate enough for making vital business decisions such as making or buying discontinuance of a particular product or a particular line of activity, pricing during the depression, export pricing, appropriate product mix, replacement of machines, sub-contracting, etc. 8. Better results When used with standard costing, it gives better results. 9. Fixation of selling price The differentiation between fixed costs and variable costs is very helpful in determining the selling price of the products or services. Sometimes, different prices are charged for the same article in different markets to meet varying degrees of competition. 10. Helpful in budgetary control The classification of expenses is very helpful in budgeting and flexible budget for various levels of activities. 11. Responsibility accounting Since under marginal costing, fixed expenses are treated as period costs, there is no arbitrary allocation of such expenses to the various departments. As such, responsibility accounting becomes more effective when it is based on marginal costing. 12. Preparing tenders Many business enterprises have to compete in the market in quoting the lowest price. Total variable cost, when separately calculated, becomes the 'floor price.' Any price above this floor price may be quoted to increase the total contribution. 13. "Make or Buy" decision Sometimes a decision has to be made whether to manufacture a component or a product or to buy it ready-made from the market. The decision to purchase it would be taken if the price paid recovers some of the fixed expenses. 14. Better presentation Management executives better understand the statements and graphs prepared under marginal costing. The break-even analysis presents the behavior of cost, sales, contribution, etc. in terms of charts and graphs. And, thus the results can easily be grasped. Disadvantages of Marginal Costing1. Difficulty of Segregation Since marginal costing is the ascertainment of marginal cost and the effect on profit of changes in the volume or type of output by differentiating between fixed costs and variable costs, it is necessary to segregate the expenses into fixed and variable items. However, it is not that easy to segregate the expenses. Most of the expenses are neither totally variable nor wholly fixed. As such, the expenses are to be separated with reasonable accuracy. Otherwise, the technique ceases to be accurate. 2. Time element ignored Fixed costs and variable costs are different in the short run, but in the long run, all costs are variable. In the long run all costs change at varying levels of operation. When new plants and equipment are introduced, fixed costs and variable costs will vary. 3. Unrealistic assumption Assumption that the sale price will remain the same at different levels of operation. In real life, they may change and give unrealistic results. 4. Difficulty in the fixation of price Under marginal costing, the selling price is fixed based on contribution. In case of cost plus contract, it is very difficult to fix price. 5. Complete information not given It does not explain the reason for the increase in production or sales. 6. Stock Valuation Apart from work-in-progress in the case of large contracts, even stocks of manufacturing concerns cannot be shown in the balance sheet by excluding fixed costs. If they are excluded, stocks of work-in-progress and finished goods would be undervalued, and to that extent, the balance sheet fails to reflect a true and fair view of the affairs of the business. 7. Significance lost In capital-intensive industries, fixed costs occupy major portions of the total cost. But marginal costs cover only variable costs. As such, it loses its significance in capital industries. 8. The problem of variable overheads Marginal costing overcomes the problem of over and under-absorbing fixed overheads. Yet there is the problem in the case of variable overheads. 9. Sales-oriented Successful business has to go in a balanced way regarding selling production functions. But marginal costing is criticized because of its over-importance to the selling function. Thus it is said to be sales-oriented. Production function is given less importance. 10. Unreliable stock valuation Under marginal costing, stock of work-in-progress and finished stock is valued at variable cost only. No portion of fixed cost is added to the value of stocks. Profit determined, under this method, is depressed. 11. Claim for loss of stock Insurance claim for loss or damage of stock based on such a valuation will be unfavorable to the business. 12. Automation Nowadays, increasing automation is leading to an increase in fixed costs. If such increasing fixed costs are ignored, the costing system cannot be effective and dependable. Marginal costing, if applied alone, will not be of much use unless it is combined with other techniques like standard costing and budgetary control. 13. Difficulty in Application The technique of marginal costing is difficult to apply in industries like shipbuilding, contracts, etc., where the value of work-in-progress is large in proportion to turnover. Thus, if fixed overheads are not included in the closing value of work-in-progress, losses on contracts may result in every year, while on completion of the contract, there may be large profits. |

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share