| |

Consumer EquilibriumEquilibrium DefinitionWhen an object is said to be in a state of equilibrium, it means that all of the forces acting on it are balanced. It is defined as the state of being at rest due to the equal action of opposing forces. The three types of equilibrium are as follows:

A product end-state user's balance refers to the number of items and services they may purchase given their present level of income and cost prices. Consumer equilibrium enables a customer to derive the greatest satisfaction from their money. When consumers decide how much goods and services to buy, it is assumed that their goal is to maximize total utility. Consumer equilibrium refers to the answer to the consumer's problem, which includes how much of various goods and services the consumer will consume. When maximizing total utility, the consumer faces various constraints. The most important is the consumer's income and the pricing of the items and services that the consumer intends to consume. The consumer's problem refers to the consumer's attempt to maximize total utility within these constraints. The Value of Consumer EquilibriumThe number of goods and services that an end-state user can purchase given their current level of income and cost prices is referred to as their balance. Consumer equilibrium denotes the level of satisfaction, indicating the highest level of satisfaction possible from their income. Consumer Equilibrium Must Be DeterminedConsider the straightforward scenario of a buyer solely interested in consuming goods 1 and 2. This consumer knows the prices of items 1 and 2 and has a predetermined income or budget for purchasing quantities of commodities 1 and 2. The consumer will buy enough goods 1 and 2 to deplete the budget for such purchases completely. The consumer equilibrium condition determines the actual quantities purchased of each good. This condition requires that the marginal utility per dollar spent on good 1 equals the marginal utility spent on good 2. If the marginal utility per dollar spent on good 1 was more than the marginal utility per dollar spent on good 2, then the marginal utility per dollar spent on good 2 would be greater. The consumer would then make more sense to buy better 1 rather than better 2. Because of the law of diminishing marginal utility, when more of good 1 is purchased, its marginal utility will eventually fall. The marginal utility per dollar spent on item 1 will eventually equal the marginal utility spent on good 2. Of course, the quantity spent on items 1 and 2 will be decided by the marginal utility per dollar spent and the consumer's budget. Assumptions

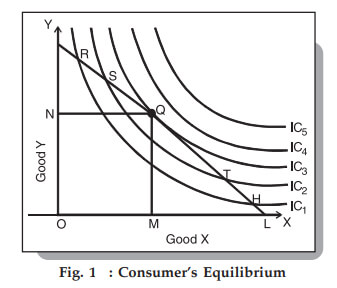

Consumers' EquilibriumBring the indifference curves and budget line together to indicate the combination of two commodities X and Y that the consumer purchases to be in equilibrium. It is something we are aware of.

The consumer pays the same price for the combinations R, S, Q, T, and H, as shown in the graph. The consumer will aim to obtain the highest indifference curve to enhance his level of enjoyment. He will be required to stay on the budget line because we have anticipated a budget constraint. Human Desires by NatureIn economics, human wants refer to a person's ambitions, aspirations, and motivations. And economic wants are those that may be satisfied with any form of product or service. Economic human wants include things like food, shelter, clothing, etc. Non-economic goals such as tranquillity, love, and affection, for example, cannot be purchased. Every person wishes to share certain basic qualities. Let us examine how human desires are comparable. Because a human is never fully pleased, his desires are limitless.

What are the Prerequisites for Achieving Consumer Equilibrium?There are certain assumptions given below for consumer equilibrium in the case of a single commodity:

In the case of consumer equilibrium for two or more commodities, we assume the following:

Consumer reaches equilibrium when the marginal benefit is received from the consumption of a commodity equals the one-unit price of the commodity. The change in a commodity's total utility is known as marginal utility. Numerically, it is written as: MU = TUn+1 - TUn MU stands for Marginal Utility in this case. Total utility is denoted by the letter TU, while n denotes the number of units consumed. When a consumer achieves equilibrium from commodity 'X consumption,' MUx = Px. Px denotes the price of one unit of commodity X, and MUx denotes the marginal utility of commodity 'X'. A rational buyer would keep buying more and more of a commodity until the marginal benefit received from it equals the price of that commodity. If a product's marginal utility exceeds its price, consumers will consume more until marginal utility falls below the price level. Similarly, if a product's marginal utility is lower than its price, consumers will cut their use until the marginal utility returns to the set price level. Utility Analysis of Consumer EquilibriumWhen a consumer buys a certain commodity and subsequently stops buying it because the price and utility have been equated. The entire utility is at its highest point at this point and the consumer is in equilibrium since he is getting the most out of the commodity and will not buy any more or less of it. This indicates that the customer has reached satiety. On the other hand, a change in price will show a result change in the quantity demanded. The formula for Consumer EquilibriumConsumer's Equilibrium is calculated as follows: Consumer's Surplus = Total Utility Obtained - Total Expenditure (At the consumer's equilibrium point) = Total Utility - Price × Quantity Purchased = Total Utility - Marginal Utility × Quantity Purchased

Next TopicLiberalization

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share