| |

What is the full form of CVVCVV: Card Verification ValueCVV stands for Card verification value. It is a set of attributes applied to credit, debit, and computerised teller device (ATM) cards to verify the cardholder's identity and reduce the likelihood of a scam. The CVV is often directed to as the card security code (CSC) or the card verification code (CVC) (CSC). Every financial institution that issues credit or debit cards has created a system where each card is given a different CVV code. Any financial transactions made with the card must be completed using this code. The PIN, which functions as a sort of password to complete card transactions, is distinct from the CVV number. The magnetic stripe on the back of your card contains CVV number, which confirms that the card is there when it is used for the transaction.

The CVV on a regular credit card consists of two parts.

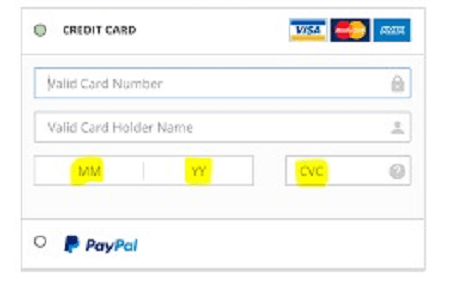

The printed CVV on a VISA, MasterCard, or Discover Card is found on the back, close to the autograph area, with three numbers. It has four digits and can be found on the front of an American Express card next to the embossed account number. The CVV is quite effective against several types of fraud when used correctly. For instance, a stripe reader will signal a "damaged card" error if the magnetic stripe's data is altered. Because it suggests that the individual submitting the order has physical possession of the card, the flat-printed CVV is (or should be) commonly required for telephone or online purchases. In addition to the bank card number, a card may optionally have a sequence of numbers called a card security code (CSC), which is imprinted or etched on the card. When a cardholder cannot physically enter a personal identification number (PIN) during a chip not spending a certain amount, the CSC is often used as a safety mechanism. We put it in place to lower the frequency of fraudulent activity.

For various card issuers, these codes are located at slightly different locations. A three-digit code to the right of the signature area on the back of Visa, Mastercard, and Discover credit cards serves as the CVV. The American Express CVV (also known as the CID or Card) is a four-digit Unique Identifier number that appears on the card's front, slightly above the account number. Michael Stone, an employee of Equifax, created CSC as an eleven-character alphanumeric code in the UK in 1995. The UK Association for Payment Clearing Services (APACS) adopted the idea after sampling it with the Littlewoods Home Shopping group and NatWest bank. It was then simplified it to the three-digit code used today. CVC2 numbers were first issued by Mastercard in 1997 and by Visa in the US in 2001. In response to increasing internet transactions and cardholder complaints of spending pauses when one questioned a card's security, American Express began using the CSC in 1999. Is a CVV and a PIN Distinct From One Another?A PIN typically has four digits, though some institutions have stricter requirements. Debit cards use PINs to make cash withdrawals and initiate purchases, while credit cards utilise them for cash advances. Both of these PINs are distinct from a CVV.

CVVs are printed on credit cards by the credit card company and are generated automatically. When your debit or credit card is printed, a bank may initially supply a PIN, but it's only momentary. You will typically be asked to alter it to a number you provide, and a CVV is not under your control in this way. CVVs: How Are They Produced?In actuality, CVVs aren't just arbitrary three- or four-digit numbers. The particular algorithms employed are unclear for apparent reasons. TypesCVV comes in a variety of forms, and all of them are generated from DES keys in the bank utilising PAN, expiration dates, and service codes: Tracks one and two of the card's magnetic stripe contain the first code, a set of three numbers known as CVC1 or CVV1. The code's objective is to confirm that the merchant genuinely holds a payment card (thus, it should differ from CVV2). This code is automatically extracted when a card's magnetic strip is read (swiped) on the device's point of sale (card present). And the issuer confirms it. A drawback is that even if you usually need to sign after that, the code is still valid if the complete card has been copied, including the magnetic stripe.

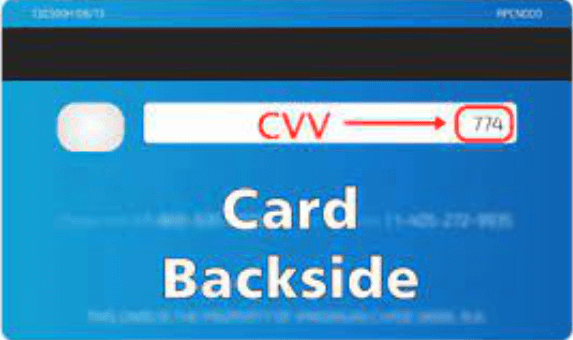

When the cardholder is not physically present, card issuers in some Western European nations demand that a merchant receive the code using the employs service number 000. For instance, it can employ the device's biometric authentication features, like Touch ID, Face ID, or pre-set passcode. Many expense approaches enable it, including Apple Pay, Google Pay, and Samsung Pay. LocationThe final three or four numbers on the signature strip on the back of the card, which are printed rather than embossed like the card digit, serve as the card security code. The card security code is printed flat rather than coded on the magnetic strip. A four-digit code is written above the number on the face of American Express cards. Benefits And Limitations

Benefits

The purpose of entering the CSC code during a transaction is to confirm that the customer possesses the card. Knowing code demonstrates that the consumer has either seen the card in person or has viewed a record created by someone who has seen the card. Limitations

How Do I Safeguard My CVV?Like any other crucial piece of financial information, your CVV should be protected if you want to prevent falling victim to credit card theft. Here are seven quick steps you may take to guard against someone getting their hands on your CVV.

Most internet transactions and other virtual payment gateways use debit and credit cards. It is against the Payment Card Industry Data Security Standards for these portals to save any data regarding the cardholder's CVV number. None can misapply the card information as a result. Due to this, using your credit card for transactions without the CVV is impossible. Dynamic CVV and EMV Chip CardsThis technology vastly improves the magnetic strip by allowing the interior regulation to modify each time the card is read. It should come as no surprise that this has significantly decreased fraudulent activities. A physical chip is useless, so your card has a CVV stamped. Even though retailers cannot digitally store CVVs, the most cunning thieves occasionally have access to them. "Dynamic CVV" is the name given to the suggested remedy for this issue because it would allow the printed code to alter after a predetermined period. This would occur on a tiny screen powered by lithium batteries and on the card's back. This might appear to be a sure thing, but despite the technology's undeniable benefits, there are some drawbacks. The frequency of the code change must be chosen carefully, and producing the cards would probably cost four to five times as much as it does now. Nevertheless, the fraud savings might more than offset the higher production costs.

As a result, additional techniques for creating dynamic CVVs have been developed, although none have attained general adoption. ConclusionCVV is something which can lock and unlock your account privacy. So, one needs to secure it strictly.

Next TopicFull Form

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share