| |

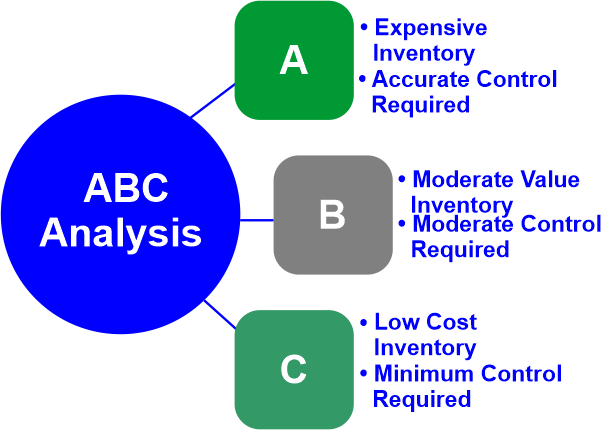

Advantages and Disadvantages of ABC AnalysisWhat does ABC analysis mean?In inventory management, the term "ABC analysis" refers to categorizing your goods according to their value to your company. The things are divided into classes A, B, and C, and the items are classified based on risk, demand, and cost. You can utilize ABC analysis to identify the inventory items that are most important and valuable for your company. The most significant SKUs are class A products, while the least considerable SKUs are class C items. Some companies divide the classification further by starting with class A products and moving up to class F.

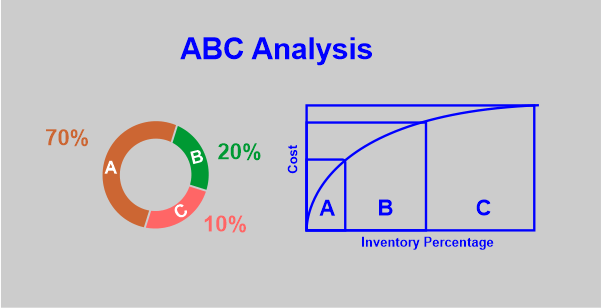

Why should a company think about applying the ABC analysis?ABC analysis allows you to understand capital costs better and maintain control over them. By doing this, you can reduce your inventory no longer needed and increase the rate at which your company's inventory is turned over. Additionally, it makes it simpler for inventory managers because they know which inventory products should take priority and which are crucial for the company's success. Inventory managers note that they have the right purchase orders because the class A items are linked to producing the highest revenue. How is the ABC inventory analyzed?Multiplying an item's annual sales by cost will get an ABC inventory analysis. You may focus your people and financial resources where they will be most effective by knowing which products are high priority & low profit. Use the formula given to analyze an ABC inventory(Estimated annual units sold) x (Item cost) = (Annual usage value per product) You can use Microsoft Excel to carry out a basic ABC inventory analysis. Indicate the value of each good or service's product consumption in decreasing order for each item. Determine the sum of each item in the total amount. Assign each item a group name after determining the values for the A, B, and C categories. The management then pays particular attention to the items with the highest value. Inventory control, 80/20 Rule, and ABC AnalysisThe Pareto Principle, often known as the 80/20 rule, states that a relatively small proportion of inventory goods account for the most utilization value. The 20% of inventory goods classified as "A" have the highest usage value, accounting for about 80% of the total usage value of the company. Items categorized as "B" comprise around 30% of the inventory and account for about 10% of the utilization value. The remaining inventory comprises items classified as "C," making only 10% of the utilization value. What is the ABC analysis process?The following are the steps in completing an ABC analysis. Step 1: Decide on your objective. To start, decide what your goal is. Do you wish to use the analysis to improve your company's cash flow? Or do you want to cut your buying costs? Make sure you carefully consider what you hope to accomplish with the analysis. Step 2: Gather the necessary data. You must get the right data to accurately classify the goods and base decisions on that. You must know each item's annual cost, and the carrying cost and gross profit margin should then be determined. Step 3: Classify using the formula. The annual utilization value for each product should be determined using the ABC analysis formula previously indicated. After completing the calculations, you should rank the items based on cost, and the most expensive products should be at the top. Step 4: Determine the effect on sales Divide the annual cost of each inventory item by the total cost of all items to get the impact on sales. Then divide this result by 100 to obtain a percentage. This is useful for comparing the different things on the list. Step 5: Arrange products into classes Defining the classes initially is the best course of action. After that, you should concentrate on the negotiation phase and then the consolidation procedure. These may reduce costs, promote savings, and guarantee that class-A objects are constantly accessible. Step 6: Perform a thorough analysis After the cost management measures have been decided, this step entails analyzing the classes. The process must include frequent reviews since they show whether the choices were good or needed to be revised. The Simplified ABC Analysis Work for Inventory ManagersInventory managers constantly look for ways to increase efficiency, raise quality, or lower prices. They might employ the ABC methodology, sometimes known as the "always better control" method, in light of that goal. They can utilize the study to devote more time and resources to Class A inventory while reducing their attention to B & C class products. Since Class A items produce the most money, inventory managers might first utilize ABC analysis to review the purchase orders for these products. Why would someone use ABC analysis?Businesses can manage their inventory based on important metrics by using ABC analysis. A company must comprehend consumer demand to ascertain whether or not its customers would purchase a specific product. Businesses that choose ABC analysis have the opportunity to assess demand & manage their inventory based on this information.

Stock optimization is another reason why organizations utilize ABC analysis. To satisfy cleansing the information, business owners can strategically establish prices for their goods or service of client needs; a business should classify its items based on demand, importance, & profit to generate a sizable amount of sales and a larger profit. Assists in identifying and reducing the number of products with low-profit margins or those customers dislike. Entrepreneurs who use the strategy get a smoother supply chain, pay less for extra stock, and effectively use their resources. Now you know how ABC analysis is used, let's move on to the advantages and disadvantages of this approach. Advantages of using ABC analysisApplying ABC analysis to inventory management can have a wide range of advantages, including:

Disadvantages of ABC AnalysisDespite its benefits for maintaining and managing inventories, ABC analysis is a more than one-size-fits-all approach. The application of an ABC study is impacted by the distinctive consumer demand patterns, classifications, systems, & other issues each organization encounters. One drawback of ABC analysis is that it focuses on the monetary value of inventory, and another is that it takes a lot of effort and discipline to apply. Other drawbacks include the following:

ABC Analysis's Benefits and Drawbacks in Brief:Benefits:

Drawbacks:

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share