| |

What is Economics?Economics is a social science that studies the production, distribution, and consumption of goods and services. It studies how individuals, businesses, and governments make choices about how to allocate resources. Economics focuses on human beings' actions, based on assumptions that humans act with rational behavior, looking for the most optimal level of benefit or utility. The building blocks of economics are the studies of labor and trade. Since there are many possible human labor applications and many different ways to acquire resources, economics determines which methods give the best results. Economics focuses on the behavior and interactions of economic agents and how economies work.

Other broad distinctions within economics include those between positive economics, describing "what is", and normative economics, advocating "what ought to be"; between economic theory and applied economics, between rational and behavioral economics; and between mainstream economics and heterodox economics. Economic analysis can be applied throughout society, in real estate, finance, health care, government and business. Economic analysis is also applied to such diverse subjects as crime, politics, law, religion, environment, and education. Branches of EconomicsEconomics is generally broken down into two categories, such as macroeconomics and microeconomics. 1. Microeconomics: It focuses on how individual consumers and firms make decisions. These individual decision-making units can be a single person, a household, a business or organization, or a government agency. Analyzing certain aspects of human behavior, microeconomics tries to explain how they respond to price changes and why they demand what they do at particular price levels. Microeconomics tries to explain how and why different goods are valued differently, how individuals make financial decisions, and how individuals best trade, coordinate, and cooperate. Microeconomics' topics range from the dynamics of supply and demand to the efficiency and costs associated with producing goods and services; they also include how labor is divided and allocated; how business firms are organized and function; and how people approach uncertainty, risk and strategic game theory. Microeconomics analyzes basic elements in the economy, including individual agents and markets, their interactions, and the outcomes of interactions. Individual agents may include households, firms, buyers, and sellers.

2. Macroeconomics: Macroeconomics studies an overall economy on both a national and international level, using highly aggregated economic data and variables to model the economy. It analyzes the economy as a system where production, consumption, saving, and investment interact, and factors affecting it: employment of the resources of labor, capital, and land, currency economic growth, inflation, and public policies that have an impact on these elements. Its focus can include a distinct geographical region, a country, a continent, or even the whole world. Its primary areas of study are recurrent economic cycles and overall economic growth and development. Topics studied include foreign trade, government fiscal and monetary policy, unemployment rates, the level of inflation and interest rates, the growth of total production output as reflected by changes in the Gross Domestic Product (GDP), and business cycles that result in expansions, booms, recessions, and depressions. Macroeconomics is intertwined. Aggregate macroeconomic phenomena are obviously and just the total of microeconomic phenomena.

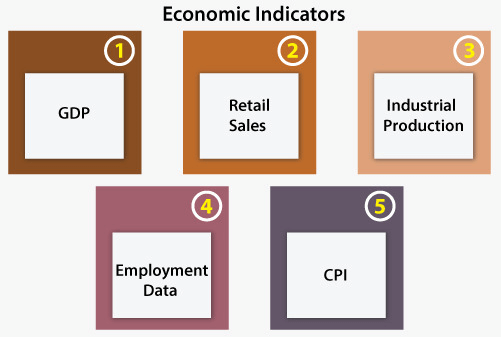

Economic IndicatorsEconomic indicators are reports that detail a country's economic performance in a specific area. These reports are usually published periodically by governmental agencies or private organizations, and they often have a considerable effect on stocks, fixed income, and forex markets when they are released. They can also be very useful for investors to judge how economic conditions will move markets and guide investment decisions. Here are some of the major U.S. economic reports and indicators used for fundamental analysis.

1. Gross Domestic Product (GDP) The GDP is considered by many to be the broadest measure of a country's economic performance. It represents the total market value of all finished goods and services produced in a country in a given period. It issues a regular report during the latter part of each month.

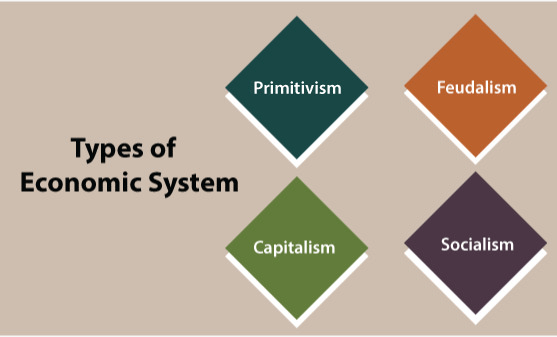

Many investors, analysts, and traders don't focus on the final annual GDP report but rather on the two reports issued a few months before: the advance GDP report and the preliminary report. This is because the final GDP figure is frequently considered a lagging indicator that can confirm a trend, but it can't predict a trend. In comparison to the stock market, the GDP report is similar to the income statement a public company reports at year-end. 2. Retail Sales As reported by the Department of Commerce during the middle of each month, the retail sales report is closely watched and measures the total receipts, dollar value, and merchandise sold in stores. The report estimates the total merchandise sold by taking sample data from retailers across the country, a figure that serves as a proxy of consumer spending levels. Because consumer spending represents more than two-thirds of GDP, this report is very useful to gauge the economy's general direction. Also, because the report's data is based on the previous month's sales, it is a timely indicator. The retail sales report content can cause above normal volatility in the market and information in the report can gauge inflationary pressures that affect Fed rates. 3. Industrial Production The industrial production report is on the changes in the production of factories, mines, and utilities in the U.S that are released monthly by the Federal Reserve. One of the closely watched measures included in this report is the capacity utilization ratio, which estimates the productive capacity used rather than standing idle in the economy. A country should see increasing values of production and capacity utilization at high levels. Capacity utilization in the range of 82-85% is considered "tight" and can increase the likelihood of price increases or supply shortages in the near term. Levels below 80% are usually interpreted as showing "slack" in the economy, which might increase the likelihood of a recession. 4. Employment Data The Bureau of Labor Statistics (BLS) releases employment data in a report called the non-farm payrolls on the first Friday of each month. Generally, quick increases in employment indicate profitable economic growth. Similarly, potential contractions may be imminent if significant decreases occur. While these are general trends, it is important to consider the current position of the economy. For example, strong employment data could cause a currency to appreciate if the country has recently been through economic troubles because the growth could be a sign of economic health and recovery. In an overheated economy, high employment can also lead to inflation, which in this situation could move the currency downward. 5. Consumer Price Index (CPI) The Consumer Price Index (CPI), also issued by the BLS, measures the level of retail price changes and is the benchmark for measuring inflation. Using a basket that represents the goods and services in the economy, the CPI compares the price changes month after month and year after year. This report is one of the more important economic indicators available, and its release can increase volatility in equity, fixed income, and forex markets. Greater than expected price increases are considered a sign of inflation, which will likely cause the underlying currency to depreciate. Economic SystemsAn economic system is the branch of economics that studies the methods and institutions by which societies determine the ownership, direction, and allocation of economic resources. An economic system of a society is the unit of analysis. Among current systems at different ends of the organizational spectrum are socialist systems and capitalist systems, in which most production occurs in state-run and private enterprises. Types of Economic SystemsSocieties have organized their resources in many different ways. Here are the following types of economic systems:

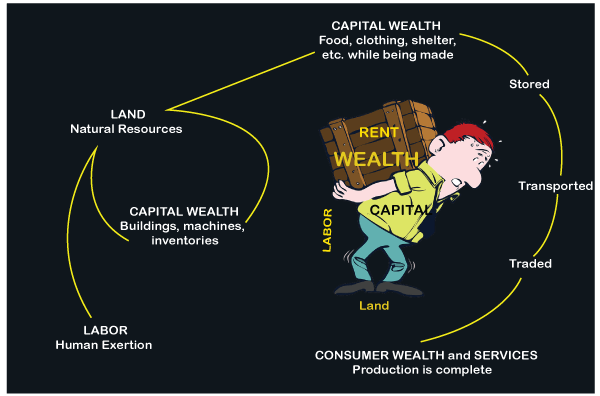

1. Primitivism In primitive agricultural societies, people tend to self-produce all their needs and wants at the household or tribe level. Families and tribes would build their dwellings, grow their crops, hunt their own game, fashion their clothes, bake their bread, etc. This economic system is defined by very little division of labor and resulting in low productivity. A high degree of vertical integration of production processes within the household or village is produced. In primitive society, the concepts of private property and decision-making over resources often apply at a more collective level of familial or tribal ownership of productive resources and wealth in common. 2. Feudalism Feudalism was a system where a class of nobility, known as lords, owned all of the lands and leased out small parcels to peasants to farm, with peasants handing over much of their production to the lord. In return, the lord offered the peasants relative safety and security, including a place to live and food to eat. 3. Capitalism Capitalism is defined as a production system whereby business owners organize productive resources, including tools, workers, and raw materials to produce goods for sale to make a profit and not for personal consumption. In capitalism, workers are hired in return for wages, landowners and natural resources are paid rents to use the resources. The owners of previously created wealth are paid interest to forgo the use of some of their wealth so that the entrepreneurs can borrow it to pay wages and rents and purchase tools for hired workers to use. Entrepreneurs apply their judgment of future economic conditions to decide what goods to produce. If they decide well, then earn a profit or if they judge poorly, then suffer losses. This market price system, profit, and loss as the selection mechanism to decide how resources are allocated for production define a capitalist economy. These roles represent functions in the capitalist economy and not separate or mutually exclusive classes of people. The United States and much of the developed world today can be described as broadly capitalist market economies. 4. Socialism Socialism is a form of a command economy. It is a production system with no private ownership of the means of production, and the system of prices, profits, and losses is not used to determine who will decide what to produce and how to produce it. Production decisions are made through some political or collective decision-making process that takes power over production resources and factors. Socialism is similar to primitivism in that collective notion of ownership and control over resources are at least nominally observed. However, in practice, it more closely resembles a feudal or slave-based economy. Those who can gain and maintain control of political power act as a privileged elite class over the workers. Communism is a variant of socialism that involves the violent overthrow of a capitalist economy and socialist economic policy. It resembles a slave-based economy where the leaders of the revolution become the new overlords or slave masters.

Next TopicWhat is Nutrition

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share