| |

Audit DefinitionAn audit is a systematic examination and verification of an organization's financial and operational records, systems, and processes. The primary objective of an audit is to determine whether the company is following established policies and procedures, adhering to laws and regulations, and accurately reporting its financial position. Audits can be performed internally, by a company's own employees, or externally, by an independent third-party auditor.

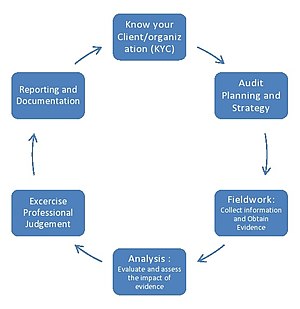

Internal audits are conducted to identify areas for improvement within the organization and to ensure that the company's internal controls are functioning effectively. These audits can cover a wide range of topics, including financial reporting, operational efficiency, risk management, and compliance with laws and regulations. External audits are typically performed by an independent auditor and are used to provide assurance to stakeholders, such as shareholders, creditors, and regulators, that the company's financial statements are accurate and free from material misstatements. The auditor reviews the company's financial records, systems, and processes and issues an opinion on the accuracy of the financial statements. The benefits of an audit include increased accountability and transparency, improved financial reporting and decision-making, and enhanced confidence among stakeholders. Audits can also help companies identify areas for improvement, reduce the risk of fraud and financial misstatements, and ensure that they are in compliance with laws and regulations. Process of auditThe audit process is a comprehensive and systematic approach to evaluating the accuracy and reliability of an organization's financial statements. The process involves several phases, including planning, risk assessment, testing, analysis, and report preparation, to provide a thorough and independent assessment of the financial health of the organization.

The audit process can be broken down into several phases: 1. Planning This is the first phase of the audit and involves the auditor assessing the risks associated with the audit, defining the audit objectives, and identifying the specific areas to be audited. This phase also involves developing an audit plan, including determining the audit timeline, assigning audit team members, and arranging access to relevant information and documentation. 2. Internal control evaluation In this phase, the auditor evaluates the internal control systems of the organization, such as its accounting procedures, to ensure that they are adequate and effective. The auditor also assesses the risk of material misstatement in the financial statements. 3. Risk assessment This phase involves the auditor evaluating the level of risk associated with specific areas of the organization's financial statements. The auditor determines which areas of the financial statements are high-risk and require more extensive testing. 4. Test of controls The auditor performs tests to determine the effectiveness of the internal control systems in place. The auditor will examine the policies and procedures in place to ensure that they are adequate, effective, and in compliance with accounting standards. 5. Substantive testing This phase involves the auditor performing tests to determine whether the financial statements are accurate and in accordance with accounting standards. The auditor will review financial transactions, balances, and disclosures to ensure that they are complete and accurate. 6. Review and analysis In this phase, the auditor analyzes the information obtained from the tests to determine whether the financial statements are free from material misstatements. The auditor also reviews any issues that were identified during the audit and decides whether to include them in the audit report. 7. Report preparation The final phase of the audit process involves the auditor preparing an audit report that summarizes the results of the audit. The audit report includes the auditor's opinion on the financial statements, a description of the scope of the audit, and any issues or findings that were identified during the audit. It is important to note that the audit process can be iterative and may involve revisiting certain phases if additional information or clarification is needed. The audit process also involves continuous communication between the auditor and the organization being audited to ensure that any questions or concerns are addressed in a timely manner. Types of auditAudits are a comprehensive examination of an organization's financial and operational records, systems, and processes. There are several different types of audits, each with its own specific objective and scope. Some of the most common types of audits include: 1. Financial Audit A financial audit is the most common type of audit and is focused on the accuracy of an organization's financial statements. The objective of a financial audit is to provide assurance to stakeholders that the financial statements are presented fairly and in accordance with relevant accounting standards. This type of audit involves a thorough review of the company's financial records, including balance sheets, income statements, and cash flow statements. 2. Operational Audit An operational audit is focused on the efficiency and effectiveness of an organization's operations. The objective of an operational audit is to identify areas for improvement and to recommend ways to increase efficiency and reduce waste. This type of audit involves a comprehensive examination of the company's processes, systems, and procedures, as well as a review of its policies, procedures, and performance metrics. 3. Compliance Audit A compliance audit is focused on an organization's compliance with laws, regulations, and other requirements. The objective of a compliance audit is to ensure that the company is adhering to relevant regulations and standards, and to identify any areas of non-compliance that need to be addressed. This type of audit involves a review of the company's policies, procedures, and internal controls, as well as an assessment of its compliance with relevant laws and regulations. 4. Information System Audit An information system audit is focused on the security and efficiency of an organization's information systems. The objective of this type of audit is to assess the effectiveness of the company's information security controls, to identify any potential security risks, and to recommend ways to improve the company's information systems. This type of audit involves a review of the company's network and computer systems, software applications, and data management processes. 5. Environmental Audit An environmental audit is focused on an organization's impact on the environment. The objective of this type of audit is to assess the company's environmental performance and to identify areas for improvement. This type of audit involves a review of the company's environmental policies, procedures, and performance metrics, as well as an assessment of its compliance with relevant environmental regulations. 6. Social Audit A social audit is focused on an organization's impact on society. The objective of this type of audit is to assess the company's social performance and to identify areas for improvement. This type of audit involves a review of the company's policies, procedures, and performance metrics, as well as an assessment of its compliance with relevant social and ethical standards. Each type of audit serves a specific purpose and has its own scope and objective. Whether focused on financial accuracy, operational efficiency, compliance, information systems, environmental impact, or social responsibility, audits provide organizations with valuable information and recommendations for improvement. By conducting regular audits, companies can ensure that they are operating efficiently, effectively, and in compliance with relevant laws and regulations. Advantages of audit1. Increased accountability and transparency Audits provide an independent and objective assessment of an organization's financial operations, helping to increase accountability and transparency in financial reporting. 2. Improved financial reporting Audits can help to identify and correct errors or inconsistencies in financial reporting, improving the accuracy and reliability of financial statements. 3. Increased public confidence The public is more likely to trust an organization that has undergone an independent audit, as the audit provides assurance that the financial statements are accurate and reliable. 4. Enhanced decision-making An audit can provide valuable insights and recommendations that can help an organization make informed decisions and improve its operations. 5. Compliance with laws and regulations Audits help organizations comply with laws and regulations related to financial reporting, such as the Sarbanes-Oxley Act, which helps to prevent financial fraud. Disadvantages of audit1. Cost Audits can be expensive, especially for smaller organizations. The cost of an audit can include the fees of the auditor, the cost of preparing for the audit, and the time and resources required to respond to audit requests. 2. Time-consuming Audits can be time-consuming, taking several months to complete. This can divert resources and attention away from the organization's core business operations. 3. Potential for conflict Audits can sometimes result in conflict between the auditor and the organization being audited. This can be due to disagreements over findings or recommendations, or over the auditor's interpretation of the data. 4. Limited scope Audits are limited in scope, and may not provide a comprehensive understanding of all aspects of an organization's operations. 5. Dependence on auditors An audit can only be as effective as the auditor conducting it. An organization may be dependent on the expertise, objectivity, and impartiality of the auditor, which may limit the value of the audit. The advantages and disadvantages of audits need to be carefully considered when deciding whether or not to conduct an audit. While audits can provide valuable insights and increase accountability and transparency, they can also be expensive, time-consuming, and potentially lead to conflict.

Next TopicConduction Definition

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share