| |

Financial AccountingFinancial accounting is a field or branch of accounting that works on the summary, analysis, and reporting of financial transactions that take place in the business. In the financial amounting, an accountant prepared the various financial statements for public use which shows the company's financial position. This information is useful for many parties who have an interest in the business like stockholders, supplies, banks, employees, business owners, Government agencies, etc. Financial accounting works by using both local and international standards.

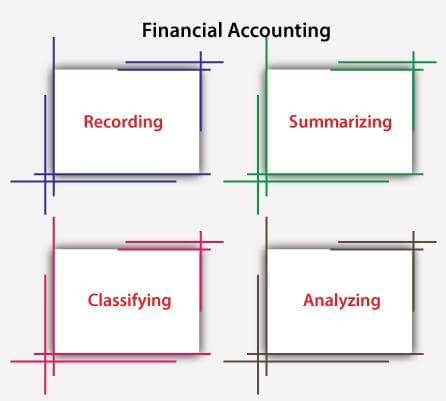

Objectives of Financial Accounting

Basic Financial StatementsThere are four basic financial statements used in financial accounting which include the following: 1. Income StatementAn income statement is a statement that shows the company's net income differing a certain period. This net income is calculated by deducting total expenses from total revenue. Numerically, it can be represented as follows: Net Income = Total Revenue - Total Expenses Sometimes, income statement is also referred to as the Profit and Loss Statement. 2. Balance SheetA balance sheet represents a company's assets (items which are owned by the company) and liabilities (items which are owed to the company) along with the shareholders' equity as of a particular date, generally prepared at the end of the financial year, i.e., 31st March. On a balance sheet, the combined balance of liabilities and equity is equal to the balance of assets. Numerically, Assets = Liabilities + Shareholders' Equity Items to be Presented on Shareholders' Equity

3. Cash Flow StatementThe cash flow statement is a document that represents the complete detail related to the income and debts off a company over a particular period. Add the name clears, the cash flow statement is related to the inflow and outflow of cash only and it does not include depreciation and amortization costs like an income statement. This statement represents the company's short-term viability by indicating the liquidity of the company or can say availability of the working capital on hand to pay the employees and debts on time. 4. Statement of Retained Earnings (Statement of Changes in Equity)It is additional statement the represents the effect of distribution of income and transfer of dividends over the wealth of the shareholders in the enterprise. Retained earnings refer to the previous year's profits that are accumulated till current period. In simpler terms, it is that part of profit which is not distributed among the shareholders and kept in the business for reinvestment. The numerical formula for calculating the retained earnings is as follows: Retained Earnings at the end of period = Retained Earnings at the beginning of period + Net Income for the period - Dividends Methods of Financial AccountingThere are two methods which a company can use to record its transactions. The company can use any one of them or a combination of both. These methods are: 1. Cash AccountingUnder this method, only cash transactions are recorded which are made by the employees of an organization. For example, if an employee is on a business trip, he/she can make cash transactions by meals and lodging and incidental expenses. After these cash transactions, the employee can report them to the manager with the receipts. These transactions are logged in the books after the approval. 2. Accrual AccountingUnder this method, all data is recorded by the book-keeper from the transactions. Accrual accounting includes the cash transactions as well as credit, debit, and other forms of payment for transactions made by employees. Because of this, accrual method is said to be an expansion of cash accounting. This category also incorporates the account payable and account receivable which can show the capital owed to by a customer. This method gives a clear picture of the company's cash flow and in determining the current assets and liabilities. Circulation of Accounting StatementsFinancial statements are often used by various parties who have an interest in the company whether they are insiders or outsiders. They include the following:

Tips for Recording Financial TransactionsIt is necessary for an accountant to be careful while recording the financial transactions. There are three tips given to reduce the possibility of any mistake: 1. Understanding the Types of AccountingIt is most important to understand both the types of financial accounting , i.e. accrual and cash accounting. It helps you in applying the specific type of financial accounting for the specific use. 2. Know which Financial Statements to UseThe need of financial statement is based on the size of your business. If you are seeking for an investor then it is good too usse all the financial statements because it shows a clear picture of company's financial status. This transparency brings a higher potential for investors to build a trust on your company. And for this balance sheet is important for them to know about the assets and liabilities of the company. 3. Apply Accounting PrinciplesAmounting principles are applied at every scenario of the accounting. These principles improves the quality of your records and efficiently register quarterly and annual costs.

Next TopicCost Accounting

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share